Abstract

The main goal of this study was to look into how SACCOs affect the economic empowerment of women in Adea Barga District, which is part of the West Shoa Zone in the Oromia Regional State, Ethiopia. The study focused on two main aspects of SACCOs: the loans and credit provided, and the dividends given to members. These factors were examined to understand their impact on women's economic empowerment. The study used both descriptive and explanatory research designs, and it followed a quantitative research approach. Probability sampling methods, specifically cluster and simple random sampling, were used to allow the researcher to choose samples from the target population with some personal judgment. A total of 36 questionnaires were used to gather primary data from 186 respondents. The data was collected through a 5-point Likert Scale questionnaire and then analyzed using SPSS Version 25. The research findings show that most employees or respondents in SACCO's Cooperative are about average in their satisfaction with Loans and Credit, and Dividend Paid to Members. The analysis results showed a strong positive and significant relationship between the dimensions of SACCO's Cooperative and the overall economic empowerment of women. The variables included in the study explained 82.1% of the variability in women's economic empowerment. Based on these findings, the researcher recommends that Adea Barga District's SACCO Cooperative should work on improving its Loans and Credit, and Dividend Paid to Members. It should also make long-term agreements with key customers to build reliability and responsiveness. The cooperative should stay informed about changing needs to better understand its partners and should focus on improving the economic empowerment of women through SACCO's Cooperative.

Keywords

SACCO’s Cooperative, Economic Empowerment of Women, Adea Barga, West Shewa

1. Background of the Study

Around the world, men have better access to saving options and banks than women. More than 70% of the poorest people are women, and two-thirds of the illiterate people in the world are women living in rural areas. One of the goals in the Sustainable Development Goals (SDGs), specifically Target 5a, is to work on changes that support women's rights when it comes to controlling money, land, and other resources.

| [21] | United Nation sustainable Development goals. 2. (2016). Target 5a of the Sustainable Development Goals. |

[21]

.

We focus on sub-Saharan Africa because this region has little research on WEE and faces the highest levels of gender inequality and poverty worldwide, especially for women

| [4] | Al-Shami, 2. (2014). Conceptual framework: The role of microfinance on the wellbeing of poor people cases studies from Malaysia and Yemen. Asian Social Science; 10(1), 230-242. https://doi.org/10.5539/ass.v10n1p230 |

[4]

. Education is seen as a key factor that affects women's empowerment through microfinance institutions in Malaysia and Yemen, but there hasn't been any real study to prove this connection.

A key part of what savings and credit cooperatives do, especially in developing countries, is their work in the microfinance and micro lending areas. This is because their members and customers often need this type of financing to invest in small businesses that can pay back the loans

| [23] | Zavala. J. D. J., B. 2. (2020). Análisis del crédito productivo de las cooperativas de ahorroy crédito en la provincia de Tungurahua. Polo Del Conocimiento: Revista científico-profesional, 5(1), 106–125. |

[23]

. In countries like Ethiopia, there's not much of a saving culture. This is due to weak stock markets, the dominance of urban-based commercial banks, and the lack of regulation for micro finance institutions in the financial system. Women in Ethiopia have fewer opportunities in the formal sector compared to men. This is probably because men have long held most leadership and management roles, which are more common in the formal sector. The informal sector, on the other hand, offers more flexibility for women who also have to manage household tasks. Because of the time pressure women face—balancing work and home responsibilities—and the belief among some leaders that men are the main earners in a family—women in Kenya and Ethiopia often earn less than men, even when they do the same jobs

| [7] | Cannon, A. 2. (2010). Life of One’s Own: Women’s: Women’s Education and Economic Empowerment in Kenya. |

[7]

. Taking these thoughts into consideration, the most important question addressed in this study was focused on to investigate the effect of SACCO’s Cooperative on Economic Empowerment of Women of West Shewa Zone, Adea Barga District, as well as to instigate efforts to fill these gaps by the concentration of Adea Barga District’s SACCO’s Cooperative. Thus, the researcher was tried to review some theoretical and empirical studies based on primary data and recommended them.

1.1. Statements of the Problem

SACCOs across Africa have encountered several challenges, such as unclear and uncertain governance that isn't clear to the members, weak oversight and auditing processes, and also a lack of or limited understanding of the members' needs when they join the institution to improve their financial situation

| [11] | ICA, 2. (2018). International definition of cooperatives and types. |

[11]

. SACCOs still play a major role in the lives of many people. These institutions collect and grow the savings of their members, then offer them loans at reasonable interest rates, which are usually lower than those provided by other financial institutions like commercial banks

| [10] | Feather, C. M. (2019). Strengthening housing finance in emerging markets. |

[10]

.

In terms of structure, cooperatives come in two types: primary and secondary. The primary ones are cooperative societies with individual members, while the secondary ones are cooperative unions, also known as SACCOs

| [24] | Zikala. M. J., 2. (2016). The role of savings and credit cooperatives in promoting access to credit in Swaziland. Research Thesis 265678, Collaborative Master’s Program in Agricultural and Applied Economics. |

[24]

. Bringing resources from within the country is essential for supporting quick economic growth and development. For a country to achieve sustainable growth, it needs a lot of savings and investments. However, in many developing countries, including Ethiopia, there is a big gap between savings and investment, which makes it hard to fund the investments needed for growth using only domestic savings. Because of this, many developing countries rely on borrowing from the government or getting loans and grants from abroad as a temporary solution.

According to a study done in Kenya

| [16] | Mudibo, E. 2. (2015). Highlights of the SACCO movement and current trends in the Kenya Union of Savings and Credit Co-operatives (KUSCCO). Nairobi: KUSCCO. |

[16]

, the main goals of Savings and Credit Cooperative Societies are to help members by encouraging savings, providing loans, and making sure the SACCOs remain financially strong through careful management. Even with government efforts and the growth of SACCOs in Kenya, smaller members still face disadvantages. The above studies were failed/lacks to demonstrate effects of SACCO cooperative on economic empowerment of women in Adea Barga District in order to economically empower them in line with Loans and Credit, and Dividend Paid to Members parametric. Therefore, to fill the above stated gaps the researcher inspired to investigate effects of SACCO cooperative on economic empowerment of women in Adea Barga District. In order to do so the researcher addressed the questions.

Therefore, the trigger issue which cause for this study is that the previous researchers’’ lacks to find research done on the effects of SACCO cooperative on economic empowerment of women in Adea Barga District as the knowledge of the researcher. So, the researcher tried to fill theoretical, geographical and empirical gap and took it as research gap on this field of study.

Taking these thoughts into consideration, the most important question addressed in this study was investigated the effects of SACCO cooperative on economic empowerment of women in Adea Barga District. Thus, the researcher reviewed some theoretical and empirical studies based on primary data and recommended them.

1.2. Research Objectives

The overall objective of the study was to investigate the “Effect of SACCOS on economic empowerment of women in Adea Barga District, West Shoa Zone, Oromia Regional State, Ethiopia”with specific objectives are here under;

1) To investigate the effects of Loans and Credit by SACCOs cooperative on economic empowerment of women in Adea Barga district.

2) To investigate the effects of Dividend Paid to Members on economic empowerment of women in Adea Barga district.

2. Review of Related Literatures

2.1. Concept of SACCOS

Savings and Credit Cooperatives, or SACCOs, are groups of people who come together to help improve their economic lives. They share the same values and principles as other cooperatives. According to International Cooperatives, a cooperative is a group of people who work together to own and control an organization that meets their social, cultural, and economic needs. SACCOs are a type of cooperative that helps members save money and also gives them access to loans

| [19] | Tadael, W. 2. (2017). Determinants of Performance of Employees Savings and Credit associations in Ethiopia: A case study of ETHIO TELE COM. (Masters Dissertation, Addis. |

[19]

. SACCOs have been very important in reducing poverty and helping people start businesses by providing better access to banking services in rural areas

| [20] | Tesfamariam, K. 2. (2015). Savings and Credit Cooperatives in Ethiopia: Development and Challenges. Journal of Economics and Sustainable Development. |

[20]

. In addition to helping people support their families, the small loans provided by SACCOs also help improve education, health, and overall quality of life for families

| [8] | Chowdhury, M. 2. (2017). The Impact of Micro Credit on Fi nancial Condition and Socio-economic of Women Entrepreneurs in Bangladesh. |

[8]

.

2.1.1. Credit/Loaning/Lending Services

Without access to finance, small-scale SACCO members can't get or take on new technologies. Even though the SACCO is the biggest and most important source of credit for its members, it is generally thought that the SACCO sector isn't getting enough support. Because of this, SACCO members depend more on non-SACCO services like their own savings, earnings, or help from family, and also on the informal sector like money lenders, since they don't have the collateral needed for loans from commercial banks

| [17] | Satta, 2. (2003). Aspects of outreach: A framework for a discussion of the social benefit. |

[17]

. Now it's widely accepted that SACCOs play a major role in the social, economic, and political development of their members and also in countries that are moving from command to market economies

| [15] | Matlay, H. P. (2005). Virtual teams and the rise of e-entrepreneurship in Europe. International Small Business Journal 12(3): 353-365. |

[15]

.

Investment is a key part of what a SACCO does. This allows members to start a business by putting their money at risk and getting a return (profit) from it. Specifically, the investment function of a SACCO includes selling shares to members in the right amounts and at the right times; using those shares to secure the savings and loans of the members, by making sure there's enough money (liquidity) in the SACCO, to manage the risk of people taking their money out or not paying back on time; keeping some of the profit made from lending to give as dividends to members based on the number of shares they own; and sharing the profits with members as dividends based on their shares

| [1] | Adera, 2. (2015). Instituting effective linkages between formal and informal financial sector in Africa: A proposal”. Savings and Development, 1/1995: 5-22. |

[1]

.

The investments made by SACCOs can be in the form of loans and/or securities. One of the basic roles of SACCOs is to help members turn financial assets that are not very useful into other types of financial assets that are more useful to them

| [3] | Allen, F. (2014). Financial Innovation and Risk Sharing, the MIT Press. |

[3]

. This transformation involves at least four economic functions: helping with the timing of money (maturity intermediation), reducing risk through diversification, lowering the cost of making deals and processing information, and providing a way to make payments. The level of investment by SACCOs is a good sign of long-term economic growth, the building up of capital, and improvements in productivity for its members. SACCOs perform roles like gathering and distributing resources, spreading out risks, and managing liquidity to help their members grow. Even in a world with full information and certainty, SACCOs can act as temporary providers of resources when there's a delay between a company's payments for inputs and the money it gets from selling its products

| [9] | Edwards, S. (2008). Real Exchange Rate, Devaluation, and Adjustment. Cambridge, Mass: MIT Press. |

[9]

.

2.1.2. Dividend Paid to Members

Dividends Paid to Members: the distribution of some of a company's earnings as cash to a class of its shareholders. Dividends typically are credited to a brokerage account or paid in the form of a dividend check. The dividend check is mailed to stockholders but can be direct-deposited to a shareholder's account of choice, if preferred.

2.1.3. Women’s Economic Empowerment

Women's economic empowerment means how well women can make, keep, and control money and things they own. It looks at what women think and do, as well as how they relate to their families, communities, and the society around them. Things like laws, rules, and policies, along with ideas about gender and social behavior, can affect how well women can earn and manage money. Women's economic empowerment is both a process and a result

| [6] | Buvinic., 2. (2020). Measuring Women’s Economic Empowerment: A Compendium of Selected Tools. Center for Global Development. |

[6]

. It has three parts: resources, choices they make, and the results they achieve.

2.2. Theoretical Review

2.2.1. The Agency Theory

In an agency relationship, one party, called the agent, makes decisions and acts on behalf of another, called the principal. The agency theory attempts to summarize and solve problems arising from the relationship between the SACCOs owners and their agents. Agency relationships are common in financial management, due to the nature of the industry

| [5] | Bhati, S. 2. (2015). Relation between trust theory and agency theory. Commerce and Management - A Modern Perspective (pp. 57-65). India: Archers and Elevators Publishing House. |

[5]

.

2.2.2. Growth of Wealth Theory

The Savings and Credit Co-operative Society (SACCOs) system is a group where members come together to save money by buying shares. These SACCOs are owned by their members, and the money saved becomes the society's wealth. The members are connected by a shared interest or goal, such as living in the same area, working in the same job, being part of the same community, or having another common link. SACCOs mainly offer savings and credit services, but they also provide other services like money transfers, payment options, insurance, and programs to help members grow.

| [13] | Maina, D. 2. (2007). Cooperative Finance: A financial Management Book for Savings and Credit Cooperatives, Kenya: Regional Institute for Cooperatives |

[13]

.

2.2.3. Empowerment Theory

| [12] | Ledwith, M. 2. (2005). Community Development. Portland: Policy Press. |

[12]

Describes empowerment as the process of having control over conditions important to people sharing similar experiences.

Working together through collective state of consciousness that promotes change and creates empowerment. Led with states “empowerment is not an alternative solution to the redistribution of unequally divided resources. Empowerment is more than providing the resources for one to help them out of poverty, it is the act of providing the necessary tools to shape the whole person and promote a critical way of thinking and consciousness.

2.2.4. Resource-based Theory

Also known as the resource-advantage theory of the firm as developed by Barney 1991 states that firms can exploit their resources in order to achieve the desired sustainable competitive advantage. He indicates that sustainability of a competitive advantage relies on the extent of exploitation of resources. Thus, the theory argues that a person’s achievements depend on the resources and capabilities they possess. These resources include human capital, physical capital, financial capital and technology. Individuals utilize the resources to build capabilities that create returns and positive impact on their lives and that of firms. Women access credit and obtain financial training among others from the savings groups which create capital, physical, and human resources. The resources obtained create important channels for women’s empowerment. The results of women empowerment include financial sustainability, ownership of assets, and contribution to household income, agency and mobility. Unfortunately, the competitive advantage aspect of the theory cannot be empirically measured in the changing dynamics of the markets and societal composition.

2.3. Empirical Literature Review

Women empowerment is a process in which women challenge the existing norms and culture, to effectively improve their well-being

| [14] | Malik, N. 2. (2005). Impact of Micro Credit on women empowerment. |

[14]

describes empowerment as “the enhancement of assets and capabilities of diverse individuals and groups to engage, influence and hold accountable the institutions which affect them”. The study further says among the different disempowered groups like: poor, ethnic, minorities etc., women are one which is cross-cutting category with all these groups.

Considered education as an intervening variable that influenced the MFI's women empowerment in Malaysia and Yemen but no empirical investigation was conducted to substantiate the relationship between the two variables he has tried to explain the various activities performing by a rural co-operative society. This is case study of Co-operative Saving and service Center Nayabazar, Bhaktapur. For analysis the data, she used simple statistical and mathematical tools. Her study concluded that: Rural cooperative in Nepal are smoothly running. The members are happy and they do not have complained against the cooperative’s management. The investment of rural cooperative is encouraging. The loan recovery of rural cooperative is satisfactory.

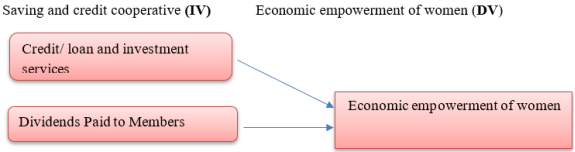

2.4. Conceptual Framework

Among different SACCO’s cooperative variables stated in the literatures reviewed, the researcher selected credit/ loan and investment services and was analyzed the effect of SACCO’s cooperative on economic empowerment of women in Adea Barga district. In this study SACCO’s cooperative variables are Independent variables and resources, agency and achievements are the Dependent variable. Accordingly, the researcher developed the following conceptual framework and indicated the relationship between the independent and dependent variables.

Figure 1. Conceptual Framework of the study developed by the researchers.

3. Research Methodology

Therefore the research design employed for this study was consists of both descriptive and explanatory research designs. The descriptive design helps to describe those data and helps to know the event that is takes place and to describe the current practices of effect of SACCO’s cooperative on economic empowerment of women by using mean and standard deviation. On the other hand, the researcher used explanatory design to examine the relationships between independent and dependent variables for aforementioned objectives and to analyze the effect of SACCO’s cooperative on economic empowerment of women by using correlation and multiple regression method.

3.1. Research Approach

To arrive on appropriate conclusion about the issue and in order to answer research objectives the necessary data was collected through quantitative research approaches. Quantitative approaches allowed the researcher to measure and analyze statistical data.

3.2. Type and Source of Data

The researcher analyzed the study based on the data collected from primary sources through questionnaire from the employees and a woman’s who are working at farming of the Adea Barga district SACCO’s cooperative. Though, the researcher used primary data to achieve the aforementioned objective and to answer research questions. Primary data were collected from selected respondents in the some purposively selected Adea Barga district SACCO’s cooperative.

3.3. Target Population

Table 1. Target population.

Identified Cooperatives | Population (Female) |

Tullu Guddina | 98 |

Abdi Boru | 78 |

Biqiltu Danse | 68 |

Talila Gorgisi | 52 |

Diddimtu | 60 |

Biftu | 33 |

Total | 389 |

The whole set of the universe from which a sample taken is called the population

| [18] | Saunders, M. L. (2007). “Research Methods For Business Students”, 4th Edition, Prentice Hall. |

[18]

. Since the main objective of this research is to find out the effect of SACCO’s Cooperative on Economic Empowerment of Women in Adea Barga District, the study area is within Adea Barga District by targeting populations of members of six (6) SACCO’s Cooperative Tullu Guddina (98), Abdi Boru (78), Biqiltu Danse (68), Talila Gorgisi (52), Diddimtu (60) and Biftu (33) among 24 SACCO’s cooperatives.

3.4. Sampling Techniques

In this study the researcher was used probability sampling technique particularly cluster and simple random sampling method to select an optimal sample size from the identified target population, because it is sampling in which one divides the elements in the population in to a number of clusters or groups. Once then begins by choosing at random a sample of these clusters, after which a simple random sample of the elements in each chosen cluster is selected. Therefore, the following table indicates the target population of SACCO’s Cooperative and total number of members of Adea Barga Distric.

3.5. Sample Size Determination

Determining sample size is very complex as it depends on other factors such as margins for errors, degree of certainty and statistical technique. A general rule, one can say that the sample must be of an optimum size i.e., it should neither be excessively large nor too small. Adea Barga SACCO’s Cooperative has more than 24 cooperatives. Among those departments, the study selected six Cooperative Tullu Guddina (98), Abdi Boru (78), Biqiltu Danse (68), Talila Gorgisi (52), Diddimtu (60) and Biftu (33).

Sample size of the researcher was calculated based on below formula (Kothari, 2004).

Where, p =proportion of success e=standard error

q =proportion of fail

N=total population

n =sample size

z= confidence level

Therefore, The researcher was used (Kothari, 2004) formula to determine the sample size for the study based on a 95% desired confidence level, a 5% desired level of precision, proportion of success (50%), proportion of fail (50%) and confidence level (1.96).

3.6. Method of Data Collection

In order to obtain relevant and adequate information the study used primary data which collected through self-administered questionnaires with close ended questionnaires as instruments of data collection, for the investigation of effect of SACCO’s Cooperative on Economic Empowerment of Women. In designing the questionnaire, a five point Likert scale would be employed to provide the extent of the respondent’s feelings or opinions on the effect of SACCO’s Cooperative on Economic Empowerment of Women.

3.7. Methods of Data Analysis

In order to establish the SACCO’s Cooperative implemented by the case organization data was analyzed using descriptive statistics where statistical tools like mean and standard deviation was used. After coding, analysis of all data was carried out using the Statistical Package for Social Science (SPSS) version 25.0. Also, inferential statistics was used to analyze the effect of SACCO’s Cooperative on Economic Empowerment of Women. Specifically, data analysis was performed using multiple regression analysis which is instrumental in demonstrating whether SACCO’s Cooperative practices considerably predict Economic Empowerment of Women.

Therefore, the model that is applied for this study was as described below:

Multiple Regression model, Y= β0 + β1 X1+ β2 X2 + e

Where:

Y = Economic Empowerment of Adea Barga district’s Women

β0 = Constant (value of Y when X1, and X2, = 0)

Β1=Regression coefficient for Loans and Credit

X1= Loans and Credit

Β2= Regression coefficient for Dividend Paid to Members

X2= Dividend Paid to Members e = the error

Thus, after testing its significance statistically, the researcher was identified the effect of SACCO’s Cooperative on Economic Empowerment of Women of the district.

4. Result and Discussion

4.1. Reliability Test

A Cronbach’s Alpha reliability test is a test which determines the internal consistency of the construct item. The reliability of the questionnaire is tested by using Cronbach’s alpha or called the alpha coefficient to show the internal consistency of questionnaires. The closer the reliability coefficient of 1.00 is the better.

The following rules of thumb: α > 0.9 Excellent, α > 0.8 Good, α>0.7 Acceptable, and α > 0.6 Questionable α > 0.5 Poor and α < 0.5 Unacceptable.

Table 2. Cronbach’s Alpha reliability test.

Variables | Number of items | Cronbach's Alpha reliability test |

Loans and Credit | 5 | 0.874 |

Dividend Paid to Members | 6 | 0.822 |

Economic Empowerment of Women | 9 | 0.818 |

Total | 36 | 0.7940.80 |

(Source: Researcher’s survey result, 2024)

As the result showed from the

Table 2 above, the researcher got the average Cronbach’s alpha coefficient that was considered as Good value because, the Alpha values of all scales could be described as the following and the overall reliability value was 0.80 which is greater than 0.70. Therefore, the reliability of the questionnaire is analyzed by using Cronbach’s alpha statistics was reliable.

4.2. Descriptive Statistical Analysis of the Study

In this part descriptive statistics in the form of mean and standard deviation were presented to illustrate the level of agreement of the respondents with their implications. The responses of the respondents for the variables indicated below were measured on five point Likert scale with: 1=strongly disagree, 2=disagree, 3=neutral, 4=agree and 5=strongly agree.

According to

| [2] | ALhakimi. W., &. 2. (2014). Internal Marketing as a Competitive Advantage in Banking Industry. Academic Journal of Management Sciences. 3(1), 15-22. |

[2]

the Likert scale response has been putted on an interval of mean based on the following formula;

Max-Min / n1 which means 5-1 / 5 = 0.80

Therefore, in the difference of 0.8 the mean value categorized from the lowest up to the highest score. It means that the scores falling between the following ranges can be considered as:

Table 3. Mean values categorization.

Mean interval | Respondents Intuition/ opinion |

1. 1.00-1.80 | Strongly Disagree (mean lowest practiced) |

2. 1.81-2.60 | Disagree (mean Lowest practiced) |

3. 2.61-3.40 | Neutral (mean averages practiced) |

4. 3.41-4.20 | Agree (mean well practiced) |

5. 4.21-5.0 | Strongly Agree (mean very well practiced) |

So, the following descriptive statistics tables of both independent and dependent variables were interpreted based on aforementioned mean value.

4.2.1. Descriptive Analysis for Economic Empowerment of Women

To measure SACCO’s cooperative on economic empowerment of women in Adea Barga district there are more than five metrics (these are; Loans and Credit, and Dividend Paid to Members parametric).

Table 4. Descriptive statistics of Economic Empowerment of Women.

Item | N | Mean | Std. Deviation |

It is ours and we are happy with SACCO even if the government cannot be able to satisfy some of the core needs, we can help ourselves. | 186 | 3.52 | 1.218 |

I become able to pay school fees for children after joining SACCO while before it was very hard | 186 | 3.31 | 1.335 |

I have managed to buy a Bicycle for home use purposes and I can afford other expenses of communication and transportation fees | 186 | 3.55 | 1.217 |

I do not suffer from paying and affording water and electricity for daily use. | 186 | 3.27 | 1.240 |

Being a member of SACCOs enable us to cover medical expenses and insurance of the household members. | 186 | 3.58 | 1.451 |

I become able to cover quality food expenses after joining SACCO and my family members cannot suffer from malnutrition. | 186 | 3.97 | 1.397 |

I am able to afford a comfortable basic home infrastructure such as own house or rent payment and sanitation infrastructure. | 186 | 3.97 | 1.397 |

I afford to pay for leisure for my family and entertain with friends | 186 | 3.98 | 1.433 |

The Loan from SACCOS enabled me to own properties | 186 | 3.93 | 1.482 |

Grand mean and stand dev. | 186 | 3.6744 | 0.86538 |

(Source: Researcher’s survey, 2024)

From the

Table 4. above, Regarding to Economic Empowerment of Women, 9 questions were asked the respondents to understand that those questions resulted in Economic Empowerment of Women. The majorities mean and standard deviation score of Economic Empowerment of Women denoted that most of the respondents were agreed to be retained and efficient in all parameters. From this result it is possible to understand that, how is the SACCO’s Cooperative performance in Adea Barga district on economic empowerment of women looks like.

Therefore, the SACCO’s Cooperative performance in Adea Barga district for its respondents was practiced quick response for product adjustment to meet customer’s requirement, reasonable time for supplier selection, to be ready for packing at the company and respond to changes in the market demand is quick and efficient in all parameters.

4.2.2. Descriptive Analysis of the SACCO’s Cooperative Performance

(i). Analysis of Loans and Credit

Table 5. Statistical analysis for Loans and Credit.

Item | N | Mean | Std. Deviation |

I am happy with the flexibility of loan repayment in terms of the installments and amount repaid at intervals. | 186 | 3.13 | 1.420 |

The Loan from SACCOS has improved my ability to meet children's education and health costs in my household. | 186 | 3.54 | 1.539 |

The current duration of loan repayment is long enough and adequate for a complete refund to be made. | 186 | 3.55 | 1.567 |

The loans are available and there is no limit to the number of time members can borrow as far as the previous loan is completely repaid | 186 | 3.63 | 1.498 |

The Loan from SACCOS enabled me to own properties at my life time. | 186 | 3.62 | 1.535 |

Grand mean and stand dev. | 186 | 3.4935 | 1.23414 |

(Source: Researcher’s survey, 2024)

From the above

Table 5, observing all the values, highest number of respondents has agreed on the loans are available and there is no limit to the number of time members can borrow as far as the previous loan is completely repaid.

Using the overall variables the Loans and Credit is implemented in the Adea Barga District SACCO cooperative of females/women’s. This is indicated by overall mean of 3.494 and standard deviation of 1.5118. This showed that Adea Barga District SACCO cooperative of females/women’s has moderate/good Loans and Credit for it’s the respondents. However, the Adea Barga District SACCO cooperative has to work to improve its relationship with the customer especially by interacting with employees’ ‘to set reliability, responsiveness, and other standards for the organization.

(ii). Analysis of Dividend Paid to Members

Table 6. Statistical analysis for Dividend Paid to Members.

Item | N | Mean | Std. Deviation |

Lower dividend rate influence women to invest for long time. | 186 | 3.16 | 1.384 |

Saving more money in SACCO influence to increase the dividend share of women | 186 | 3.42 | 1.586 |

There are many rewards for those who has high dividend share. | 186 | 3.13 | 1.544 |

I feel my efforts are rewarded the way they should be. | 186 | 3.76 | 1.577 |

Employees who hold more dividend share by working hard are having getting the chance of prizes. | 186 | 3.70 | 1.623 |

Having an a dividend share in SACCO contributed to generate your income at good level | 186 | 3.85 | 1.604 |

Grand mean and stand dev. | 186 | 3.502 | 1.13138 |

(Source: Researcher’s survey, 2024)

Based on the analysis, the result of the mean value of Dividend Paid to Members scores were greater than 3.503. The value of overall mean for Contingent Rewards 3.503 suggesting that there is good Dividend Paid to Members in the Adea Barga District SACCOS.

4.3. Inferential Analysis of the Study

In this section, correlation analysis of variables, analytical tests (Multicollinearity test, and multi linear regression analysis (model summary, ANOVA and coefficients) would be stated and interpreted by using SPSS version 25 software.

4.3.1. Correlation Analysis

Table 7. Correlation matrix between constructs of IV and DV.

Correlations | Economic Empowerment of Women |

Loans and Credit | Pearson Correlation | 0.717** |

Sig. (2-tailed) | .000 |

Dividend Paid to Members | Pearson Correlation | 0.669 |

Sig (2-tailed) | .000 |

(Source: Researcher’s survey result, 2024)

(Source: Researcher’s survey result, 2024)

Correlation Matrix among SACCO’s Cooperative on Economic Empowerment of Women.

Range of value for Pearson’s coefficient (r) Level of Association/relationship r = 0.10 to 0.29 or r = -0.10 to -0.29 Small r = 0.30 to 0.49 or r = -0.30 to -0.49 Medium r = 0.50 to 1.00 or r = -0.50 to -1.00 Large |

As the correlation matrix

Table 7, above shown, the correlation coefficient values of the independent variables, Loans and Credit, and Dividend Paid to Members parametric) with the dependent variable (i.e. Economic empowerment of women) were 0.717**, 0.669. Their significant level is 0.000.

Consequently, a Pearson correlation analysis results indicated here under is a significant correlation between all independent variables, Loans and Credit, and Dividend Paid to Members parametric) with the dependent variable (i.e. Economic empowerment of women) of SACCOS in the study area, which means they have a strong effect on Economic empowerment of women.

4.3.2. Analytical Tests

Table 8. Multicollinearity Test.

Coefficientsa |

Model | Collinearity Statistics |

Tolerance | VIF |

Loans and Credit | .566 | 1.765 |

Dividend Paid to Members | .604 | 1.656 |

a. Dependent Variable: Economic Empowerment of Women |

(Source: own survey result, 2024)

4.3.3. Multiple Linear Regression Analysis

(i). Model Summary

Table 9. Model Summary.

Model Summaryb |

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Change Statistics | Durbin-Watson |

R Square Change | F Change | df1 | df2 | Sig. F Change |

1 | .906a | .821 | .816 | .37154 | .821 | 164.723 | 5 | 180 | .000 | .841 |

a. Predictors: (Constant), Dividend Paid to Members, Loans and Credit |

b. Dependent Variable: Economic Empowerment of Women |

(Source: Own Survey, 2024)

(ii). ANOVA Test

Table 10. ANOVA Test.

ANOVAa |

Model | Sum of Squares | df | Mean Square | F | Sig. |

1 | Regression | 113.696 | 5 | 22.739 | 164.723 | .000b |

Residual | 24.848 | 180 | .138 | | |

Total | 138.544 | 185 | | | |

a. Dependent Variable: Economic Empowerment of Women |

b. Predictors: (Constant), Dividend Paid to Members, Loans and Credit |

(Source: Own Survey, 2024)

(iii). Regression Coefficients

Standardized regression coefficients are useful when you want to compare the effect that different predictor variables have on a response variable. Since each variable is standardized, you’re able to see which variable has the greatest effect on the response variables.

Table 11. Regression Coefficients.

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. |

B | Std. Error | Beta |

1 | (Constant) | .217 | .126 | | 1.714 | .088 |

Loans and credit | .158 | .029 | .225 | 5.364 | .000 |

Dividend Paid to Members | .148 | .031 | .194 | 4.764 | .000 |

(Source: Own Survey, 2024)

Unstandardized regression coefficients are useful when you want to interpret the effect that a one-unit change on a predictor variable has on a response variable without comparing in terms of effect on the dependent variable

| [22] | Zach, B. (2020). Standardized vs. Unstandardized Regression Coefficients. |

[22]

.

5. Summary, Conclusion and Recommendation

5.1. Summary of Major Findings

The study was attempted to cover the effect of independent variables (i.e. Loans and Credit and Dividend Paid to Members parametric) on dependent variable (i.e. Economic empowerment of women).

Data for the study was obtained through distribution of questionnaires to a pre-determined sample of SACCO’s Cooperative of Women of West Shewa Zone, Adea Barga District. From the total distributed survey questionnaire, 95% were returned. An overall value of Cronbach alpha (a =0.7940.80) was obtained.

Through the descriptive statistical analysis, an overall mean score was computed for each independent variable (SACCO’s Cooperative). The study revealed that Dividend Paid to Members (M=3.503, SD= 1.1313), Loans and Credit (M=3.494, SD= 1.234).

The correlation analysis was done by using Pearson correlation coefficients to determine and obtain information about the relationships between the independent variables (i.e. Loans and Credit and Dividend Paid to Members parametric) and dependent variable (i.e. Economic empowerment of women). The study revealed that there is a positive and statistically significant relationship between each independent variable and the dependent variable.

The study also further discovered from Pearson correlation analysis that the relationship between each independent variable and the dependent variable according to magnitude of correlation. Multiple regression analysis was used to determine whether the independent variables influence the dependent variable. R square value from the regression model summary (R2 =0.821) indicated that 82.1% of the variation in the Economic empowerment of women can be explained by the Loans and Credit and Dividend Paid to Members as of the independent variables included in the model.

The ANOVA test result revealed that the independent variables statistically and significantly predict the dependent variable (F = 164.723, p <.001). Coming to the variable under study the regression analysis result further revealed that the predictor variables of independent variables are statistically significant in predicting Economic empowerment of women because all their p-values are less than alpha level of 0.05 and the respondents provide positive responses regarding to the effect of Loans and Credit (standardized beta coefficients are 0.225, p=0.000, and Dividend Paid to Members (standardized beta coefficients are 0.194, p=0.000) on Economic empowerment of women. From the above regression analysis Loans and Credit and Dividend Paid to Members makes the strongest unique contribution to explaining the dependent variable (Economic empowerment of women).

5.2. Conclusions

The main objective of the study was to investigate the effect of independent variables (i.e. Loans and Credit and Dividend Paid to Members parametric) on dependent variable (i.e. Economic empowerment of women). Based on the findings, the researcher concludes that SACCO’s Cooperative in Adea Barga district was moderately implemented the independent variables (i.e. Loans and Credit and Dividend Paid to Members. These practices have helped SACCO’s Cooperative in Adea Barga district to improve its member’s satisfaction.

From the result of the analysis it was concluded that there was strong positive and significant correlation between dimensions of SACCO’s Cooperative (i.e. Loans and Credit and Dividend Paid to Members parametric) and Economic empowerment of women since the SACCO’s Cooperative variables included in this study explained by 82.1% of the variability of the Economic empowerment of women.

The findings from the Pearson correlation analysis results revealed that there is a positive and significant correlation between the aggregated SACCO’s Cooperative variables and Economic empowerment of women of the Adea Barga district. Accordingly, the multiple regression analysis result of this study demonstrated that, all independent variables (designated SACCO’s Cooperative (i.e. Loans and Credit and Dividend Paid to Members has a positive and statistically significant effect on Economic empowerment of women. From the model summary of multiple regressions, the result showed that, the designated SACCO’s Cooperative variables were highly influences Economic empowerment of women.

5.3. Recommendations

Based on the findings and conclusions of the study, the researcher forwards the following recommendations. The researcher also gave a recommendation to get better their SACCOS Cooperative strategy and benefit in order to boost their members’ dedication that would enable commitment, while efficiently deliver outstanding results. Consequently, the researcher suggests for top management of the SACCO’s Cooperative of the Adea Barga district to provide satisfactory level of skill development trainings and reward for its SACCOS members based on their performance to gain competitive advantage from other SACCO’s cooperatives and to keep/retain their members for long period of time.

Based on the findings, the researcher recommended that, SACCO’s Cooperative of the Adea Barga district ought to strive to involve and improve its loans and credit benefit, and rewards as well for its SACCOS members to create long term agreement with key customers to set reliability, responsiveness, and other standard work for the organization, to be informed on the changing needs in order to improve their understanding with their trading partners and to work on improving economic empowerment of women.

The overall SACCO’s Cooperative of economic empowerment of women was neutral; this means that they were moderately satisfied. So that the researcher recommended that it is better if SACCO’s Cooperative of the Adea Barga district management give high attention to their members to satisfy them in order to achieve the organization goal. Since with low SACCO’s Cooperative members/employees’ motivation and satisfaction level, it is very difficult to be a world class industry.

5.4. Suggestions for Future Research

The study depicted the extent of adopting of effect of independent variables (i.e. Loans and Credit and Dividend Paid to Members parametric) on dependent variable (i.e. Economic empowerment of women). The findings were only relied on data provided by the case SACCO’s Cooperative of the Adea Barga district. Thus, further studies are needed to broaden the scope of respondents by incorporating more respondents who are the males, customers and suppliers of the case SACCO’s Cooperative. As the concept of SACCO’s Cooperative effects on Economic empowerment of women is very wide and involves various dimensions, it is almost impossible to cover all these dimensions in just one study. Therefore, further study would be required to cover other dimensions of SACCO’s Cooperative which are implemented by the case areas and not included in this study. Furthermore, future studies should consider barriers and challenges that impede the effective implementation of identifying the effect of extra variables/ parametric of SACCO’s Cooperative on Economic empowerment of women.

Abbreviations

SPSS | Statistical Package for Social Science |

SACCO’S | Saving and Credit Cooperatives Societies |

WEE | Women’s Economic Empowerment |

SD | Standard Devation |

Author Contributions

Jabessa Tesfa Deressa is the sole author. The author read and approved the final manuscript.

Conflicts of Interest

The author declares no conflicts of interest.

References

| [1] |

Adera, 2. (2015). Instituting effective linkages between formal and informal financial sector in Africa: A proposal”. Savings and Development, 1/1995: 5-22.

|

| [2] |

ALhakimi. W., &. 2. (2014). Internal Marketing as a Competitive Advantage in Banking Industry. Academic Journal of Management Sciences. 3(1), 15-22.

|

| [3] |

Allen, F. (2014). Financial Innovation and Risk Sharing, the MIT Press.

|

| [4] |

Al-Shami, 2. (2014). Conceptual framework: The role of microfinance on the wellbeing of poor people cases studies from Malaysia and Yemen. Asian Social Science; 10(1), 230-242.

https://doi.org/10.5539/ass.v10n1p230

|

| [5] |

Bhati, S. 2. (2015). Relation between trust theory and agency theory. Commerce and Management - A Modern Perspective (pp. 57-65). India: Archers and Elevators Publishing House.

|

| [6] |

Buvinic., 2. (2020). Measuring Women’s Economic Empowerment: A Compendium of Selected Tools. Center for Global Development.

|

| [7] |

Cannon, A. 2. (2010). Life of One’s Own: Women’s: Women’s Education and Economic Empowerment in Kenya.

|

| [8] |

Chowdhury, M. 2. (2017). The Impact of Micro Credit on Fi nancial Condition and Socio-economic of Women Entrepreneurs in Bangladesh.

|

| [9] |

Edwards, S. (2008). Real Exchange Rate, Devaluation, and Adjustment. Cambridge, Mass: MIT Press.

|

| [10] |

Feather, C. M. (2019). Strengthening housing finance in emerging markets.

|

| [11] |

ICA, 2. (2018). International definition of cooperatives and types.

|

| [12] |

Ledwith, M. 2. (2005). Community Development. Portland: Policy Press.

|

| [13] |

Maina, D. 2. (2007). Cooperative Finance: A financial Management Book for Savings and Credit Cooperatives, Kenya: Regional Institute for Cooperatives

|

| [14] |

Malik, N. 2. (2005). Impact of Micro Credit on women empowerment.

|

| [15] |

Matlay, H. P. (2005). Virtual teams and the rise of e-entrepreneurship in Europe. International Small Business Journal 12(3): 353-365.

|

| [16] |

Mudibo, E. 2. (2015). Highlights of the SACCO movement and current trends in the Kenya Union of Savings and Credit Co-operatives (KUSCCO). Nairobi: KUSCCO.

|

| [17] |

Satta, 2. (2003). Aspects of outreach: A framework for a discussion of the social benefit.

|

| [18] |

Saunders, M. L. (2007). “Research Methods For Business Students”, 4th Edition, Prentice Hall.

|

| [19] |

Tadael, W. 2. (2017). Determinants of Performance of Employees Savings and Credit associations in Ethiopia: A case study of ETHIO TELE COM. (Masters Dissertation, Addis.

|

| [20] |

Tesfamariam, K. 2. (2015). Savings and Credit Cooperatives in Ethiopia: Development and Challenges. Journal of Economics and Sustainable Development.

|

| [21] |

United Nation sustainable Development goals. 2. (2016). Target 5a of the Sustainable Development Goals.

|

| [22] |

Zach, B. (2020). Standardized vs. Unstandardized Regression Coefficients.

|

| [23] |

Zavala. J. D. J., B. 2. (2020). Análisis del crédito productivo de las cooperativas de ahorroy crédito en la provincia de Tungurahua. Polo Del Conocimiento: Revista científico-profesional, 5(1), 106–125.

|

| [24] |

Zikala. M. J., 2. (2016). The role of savings and credit cooperatives in promoting access to credit in Swaziland. Research Thesis 265678, Collaborative Master’s Program in Agricultural and Applied Economics.

|

Cite This Article

-

APA Style

Deressa, J. T. (2026). Effect of Saving and Credit Cooperatives (Sacco’s) on Economic Empowerment of Women in the Case of Adea Barga, Oromia Regional State, Ethiopia. American Journal of Theoretical and Applied Business, 12(1), 15-27. https://doi.org/10.11648/j.ajtab.20261201.12

Copy

|

Copy

|

Download

Download

ACS Style

Deressa, J. T. Effect of Saving and Credit Cooperatives (Sacco’s) on Economic Empowerment of Women in the Case of Adea Barga, Oromia Regional State, Ethiopia. Am. J. Theor. Appl. Bus. 2026, 12(1), 15-27. doi: 10.11648/j.ajtab.20261201.12

Copy

|

Download

AMA Style

Deressa JT. Effect of Saving and Credit Cooperatives (Sacco’s) on Economic Empowerment of Women in the Case of Adea Barga, Oromia Regional State, Ethiopia. Am J Theor Appl Bus. 2026;12(1):15-27. doi: 10.11648/j.ajtab.20261201.12

Copy

|

Download

-

@article{10.11648/j.ajtab.20261201.12,

author = {Jabessa Tesfa Deressa},

title = {Effect of Saving and Credit Cooperatives (Sacco’s) on Economic Empowerment of Women in the Case of Adea Barga, Oromia Regional State, Ethiopia},

journal = {American Journal of Theoretical and Applied Business},

volume = {12},

number = {1},

pages = {15-27},

doi = {10.11648/j.ajtab.20261201.12},

url = {https://doi.org/10.11648/j.ajtab.20261201.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtab.20261201.12},

abstract = {The main goal of this study was to look into how SACCOs affect the economic empowerment of women in Adea Barga District, which is part of the West Shoa Zone in the Oromia Regional State, Ethiopia. The study focused on two main aspects of SACCOs: the loans and credit provided, and the dividends given to members. These factors were examined to understand their impact on women's economic empowerment. The study used both descriptive and explanatory research designs, and it followed a quantitative research approach. Probability sampling methods, specifically cluster and simple random sampling, were used to allow the researcher to choose samples from the target population with some personal judgment. A total of 36 questionnaires were used to gather primary data from 186 respondents. The data was collected through a 5-point Likert Scale questionnaire and then analyzed using SPSS Version 25. The research findings show that most employees or respondents in SACCO's Cooperative are about average in their satisfaction with Loans and Credit, and Dividend Paid to Members. The analysis results showed a strong positive and significant relationship between the dimensions of SACCO's Cooperative and the overall economic empowerment of women. The variables included in the study explained 82.1% of the variability in women's economic empowerment. Based on these findings, the researcher recommends that Adea Barga District's SACCO Cooperative should work on improving its Loans and Credit, and Dividend Paid to Members. It should also make long-term agreements with key customers to build reliability and responsiveness. The cooperative should stay informed about changing needs to better understand its partners and should focus on improving the economic empowerment of women through SACCO's Cooperative.},

year = {2026}

}

Copy

|

Download

-

TY - JOUR

T1 - Effect of Saving and Credit Cooperatives (Sacco’s) on Economic Empowerment of Women in the Case of Adea Barga, Oromia Regional State, Ethiopia

AU - Jabessa Tesfa Deressa

Y1 - 2026/01/20

PY - 2026

N1 - https://doi.org/10.11648/j.ajtab.20261201.12

DO - 10.11648/j.ajtab.20261201.12

T2 - American Journal of Theoretical and Applied Business

JF - American Journal of Theoretical and Applied Business

JO - American Journal of Theoretical and Applied Business

SP - 15

EP - 27

PB - Science Publishing Group

SN - 2469-7842

UR - https://doi.org/10.11648/j.ajtab.20261201.12

AB - The main goal of this study was to look into how SACCOs affect the economic empowerment of women in Adea Barga District, which is part of the West Shoa Zone in the Oromia Regional State, Ethiopia. The study focused on two main aspects of SACCOs: the loans and credit provided, and the dividends given to members. These factors were examined to understand their impact on women's economic empowerment. The study used both descriptive and explanatory research designs, and it followed a quantitative research approach. Probability sampling methods, specifically cluster and simple random sampling, were used to allow the researcher to choose samples from the target population with some personal judgment. A total of 36 questionnaires were used to gather primary data from 186 respondents. The data was collected through a 5-point Likert Scale questionnaire and then analyzed using SPSS Version 25. The research findings show that most employees or respondents in SACCO's Cooperative are about average in their satisfaction with Loans and Credit, and Dividend Paid to Members. The analysis results showed a strong positive and significant relationship between the dimensions of SACCO's Cooperative and the overall economic empowerment of women. The variables included in the study explained 82.1% of the variability in women's economic empowerment. Based on these findings, the researcher recommends that Adea Barga District's SACCO Cooperative should work on improving its Loans and Credit, and Dividend Paid to Members. It should also make long-term agreements with key customers to build reliability and responsiveness. The cooperative should stay informed about changing needs to better understand its partners and should focus on improving the economic empowerment of women through SACCO's Cooperative.

VL - 12

IS - 1

ER -

Copy

|

Download